CTT Correios de Portugal: An Undervalued Growth Story with Hidden Assets trading at 8x EBIT

My latest investment is CTT Correios de Portugal SA, an €800 million small-cap company with some hidden gems within its business. It is best known for its postal mail service, originally founded in 1520 by King Manuel I of Portugal. As one might expect, traditional mail is a declining industry, and CTT's Mail segment has seen a 70% decline in mail volume since its peak in the early 2000s.

However, this is not the reason I find CTT an attractive investment. The key driver of my interest is the new management team that took over the company a few years ago. Under their leadership, CTT has been successfully expanding into high-growth business segments that are rapidly transforming the company’s future.

CTT’s future is being shaped by three key business segments:

Express & Parcels (E&P) Segment

Banking Segment

Financial Services Segment

Among these, the most important for the company's future is Express & Parcels (E&P).

Express & Parcels

CTT's E&P business is designed to capitalize on the booming e-commerce market, leveraging its existing mail infrastructure for efficient logistics. The company is Portugal’s dominant last-mile delivery provider, with an estimated market share of over 50%. Additionally, through a recent acquisition, CTT has become a significant player in Spain, now holding over a 15% market share there.

What makes this segment particularly exciting is its rapid growth and improving margins. In Q3 2024, CTT reported an 8.7% EBIT margin, and management expects even stronger performance in the next quarter as economies of scale continue to drive profitability.

Future prospects:

The e-commerce logistics industry in Portugal has significant room for expansion, as the country lags behind markets like the UK and the US in e-commerce penetration. While predicting future growth rates is difficult, I believe this industry should grow at a strong pace over the coming years.

Beyond organic growth, CTT has been aggressively expanding through acquisitions, making strategic moves to strengthen its market position.

Strategic Acquisitions & Partnerships

CTT recently acquired Cacesa, a Spanish e-commerce logistics company specializing in customs clearance and deliveries. This is a highly strategic acquisition for several reasons:

It serves as a gateway into the Spanish e-commerce delivery market.

By integrating customs clearance capabilities, CTT can offer seamless end-to-end logistics to e-commerce businesses, reducing friction for customers.

Cacesa has been growing rapidly, with €92 million in revenue and €20 million in EBIT in 2023, doubling in size over the past two years.

CTT acquired Cacesa for just €104 million, which equates to 5.5x EBIT—an extremely attractive valuation considering its growth profile.

CTT also announced a partnership with DHL, one of the world’s leading logistics companies. As part of this deal:

CTT exchanged 25% of CTT Express for 25% of DHL’s B2B segment in Spain and 100% of DHL’s Portuguese B2B operations.

DHL will also pay €69 million to CTT.

While DHL has struggled in Portugal, CTT’s local expertise could help improve performance. This partnership brings together DHL’s global logistics strength with CTT’s domestic dominance.

If the Express & Parcels segment maintains its current growth trajectory, estimated full-year 2024 revenue should reach ~€460 million. Assuming an 8% EBIT margin (pre-acquisition) and the added impact of Cacesa’s EBIT the segment could generate ~€60 million in EBIT. Applying a 13x EBIT multiple (for reference, CTT Express was valued at 12.5x EBIT in the DHL deal), this segment alone could be worth CTT’s entire market cap. I believe there is still additional upside when considering future growth and possible acquisition synergies, which management believes there should be lots of.

CTT Banco – A fast growing Bank

When the new management took over CTT a few years ago, they inherited a small, unprofitable bank. Since then, they have successfully scaled CTT Banco from €1 billion in deposits to €4 billion, while also improving ROTE (Return on Tangible Equity) to 12.4% in the latest quarter.

This rapid growth was driven by an excellent strategic move:

Management leveraged the 500-year-old CTT brand, which enjoys strong public trust.

Instead of opening costly new branches, they integrated banking services into existing service points, utilizing the pre-existing infrastructure from their Express & Parcels (E&P) and mail business.

This approach allowed the bank to expand without major capital expenditures, making growth highly efficient.

Looking ahead, CTT Banco plans to expand further into financial services, such as insurance, which could provide additional revenue streams.

Despite impressive deposit growth, profitability has lagged in recent years, mainly due to the exit from the credit card business in 2023 and the slow allocation of deposits, with a large portion sitting in low-yielding central bank reserves. However, this situation has been improving. At the end of 2023, the bank had €3.1 billion in deposits, but €1.4 billion was parked in the central bank, earning only 2–4% annually. By September 2024, deposits had grown to €4 billion, and allocation had become much more efficient, with only €800 million kept in central bank reserves, while €800 million was allocated to consumer loans (car loans & mortgages) and €2.5 billion to debt securities, mostly sovereign foreign debt. This setup appears well-structured for future equity growth, striking a balance between profitability and risk management without excessive aggression.

Currently, CTT Banco has €270 million in equity. A conservative valuation at 1x book would make the value of the bank over 30% of the market cap. Considering its growth potential and improving profitability that is probably quite conservative. Additionally, management has stated that they plan to reduce CTT’s ownership of the bank to below 50% to ensure the group’s balance sheet isn’t influenced by banking operations. This divestment could unlock significant cash flows for shareholders in the future.

Some risks need to be considered, with the most significant being the potential outflow of deposits. The rapid growth in deposits raises concerns about how sticky these deposits truly are. Since most of the new deposits have been in the form of term deposits (i.e., savings accounts), if interest rates decline or some other bank offers better yields, there is a risk of a swift outflow of deposits.

Financial Services Segment: Wild Card with potential

This segments primary service offered is public debt placements. This service allows individuals to subscribe to government-issued debt, enabling them to earn interest. In 2022 and early 2023, this was an attractive alternative to savings accounts, as interest rates had risen while the interest paid on savings accounts had not yet caught up. During this period, public debt placements offered significantly better yields compared to other risk-free alternatives.

From the graph provided, we can observe a substantial boom in public debt placements during 2022 and 2023, followed by a sharp decline in late 2023. This decline was primarily due to two factors: first, savings deposit accounts began offering competitive interest rates, and second, the Portuguese government imposed a ceiling of €50,000 per customer on these placements, as they were reluctant to issue more debt at higher interest rates. However, there has been some recovery in 2024, particularly after the ceiling was raised to €100,000 in October. Public debt placements tend to perform best when savings accounts are not offering attractive yields.

While this segment has experienced a significant dip in revenue, the margins remain strong. Looking ahead, if the caps on subscriptions per customer are raised further and yields provided by savings accounts decline, we could see a recovery in this segment. Such a recovery could make a substantial contribution to the business. If the segment returns to levels seen before the interest rate hikes in 2021/2022, it could easily contribute €20 million in EBIT. Applying a conservative multiple of 10x EBIT, this segment could be valued at around €200 million or 25% of the market cap .

Hidden real estate portfolio

CTT’s real estate portfolio, which is another intriguing aspect of the company. In their annual report, it’s noted that buildings and constructions are depreciated over a period of 10 to 50 years. While this is standard accounting practice, it’s particularly fascinating in the context of CTT, given its 500-year history. Over time, the company has accumulated real estate and constructions worth €340 million. However, due to depreciation, the book value of these assets currently stands at just €100 million. While this €100 million is still a notable portion of the company’s market capitalization, it likely underrepresents the true market value of the real estate.

On October 31, 2022, CTT took a strategic step by establishing a subsidiary called CTT IMO Yield to manage most of its real estate portfolio. In early 2023, CTT sold 26% of this subsidiary for €36 million, implying a total valuation of €137 million for this subsidiary. According to the press release, this transaction was made with the expectation that Sierra, the acquiring company, could enhance the value of the portfolio through better management and optimization.

This transaction suggests that CTT’s management believes this real estate portfolio has significant untapped potential. The €137 million valuation likely represents a conservative estimate, and there is room for further value creation as Sierra works to optimize the portfolio. This could involve redeveloping properties, leasing underutilized spaces, or even selling certain assets at higher market values.

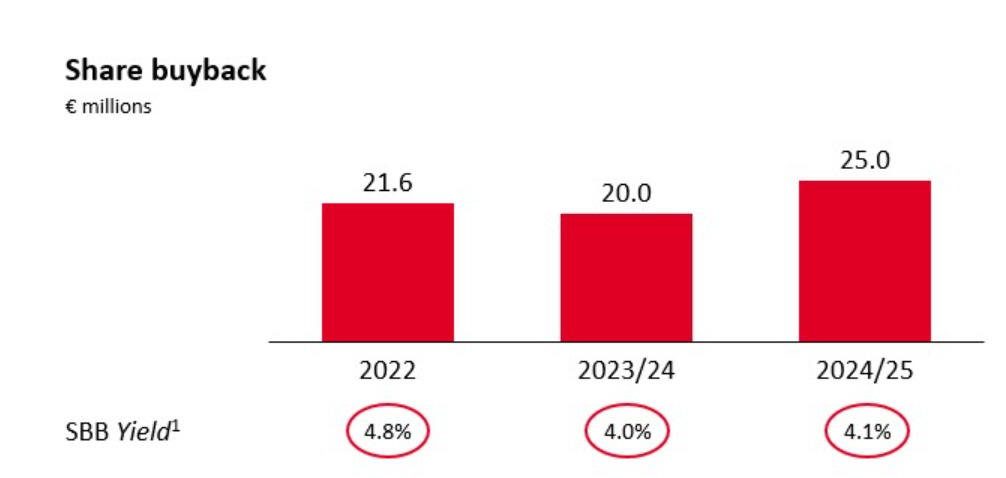

Things all shareholders like to see:

All things considered, I believe the investment case for CTT is clear. Even without significant growth, the company appears undervalued based on its existing assets and operations. However, if its key business segments continue to expand, the upside potential becomes even more compelling.

I’d like to thank @Symmetry_Invest on X for bringing this idea to my attention. Their write-up on CTT is incredibly detailed, and I highly recommend reading it for anyone interested in diving deeper into the company.