SuperCom: Nano cap disruptor with 80% underlying growth hidden by skewed accounting, while trading at 4x EBITDA

Today’s stock, and in my belief one of the most attractive setups in the market currently, is SuperCom. In short, SuperCom is a newer player in the Offender Electronic Monitoring market that is finally hitting an inflection point. Essentially, they sell and rent out the hardware and software used to track offenders. This includes the GPS wristbands and ankle bracelets used when someone is put under house arrest or parole.

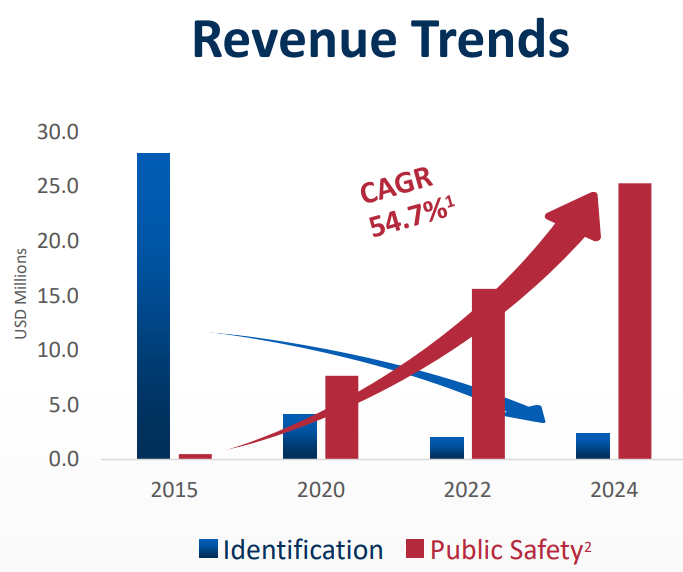

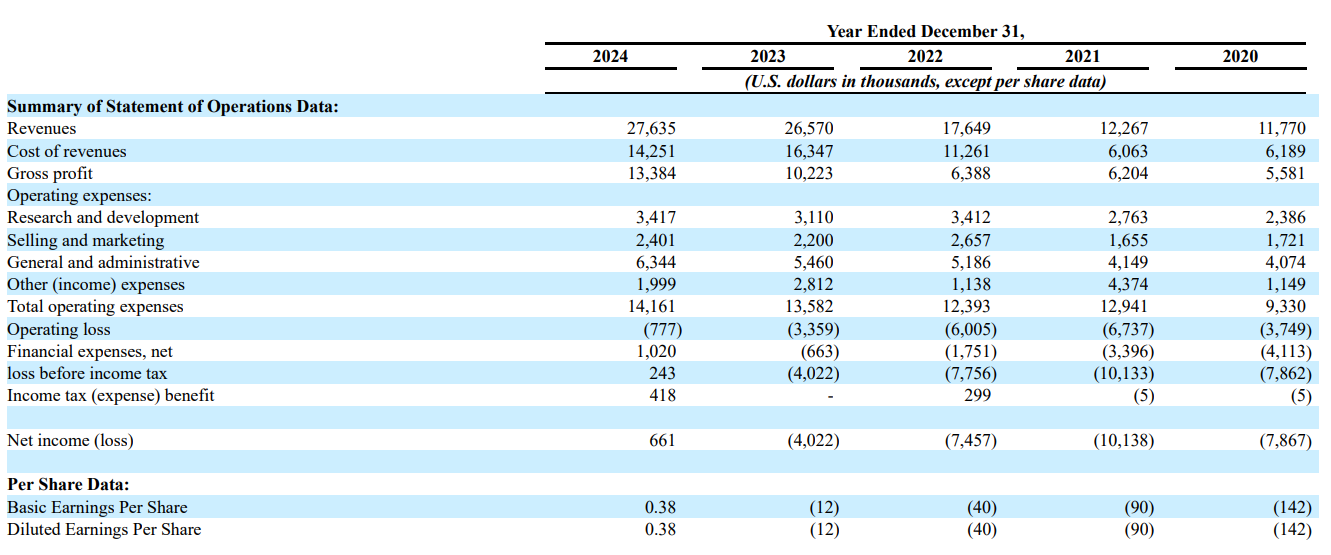

The investment appeal of SuperCom is due to its strong growth potential and low valuation. Between 2021 and 2024, the company achieved a CAGR of ~30%, which is remarkably fast for this industry. While 2025 revenue growth appeared flat or slightly negative, I believe the underlying business is actually expanding rapidly at roughly 80% year over year. The current growth is hidden behind skewed revenue figures reported in 2023 and 2024.

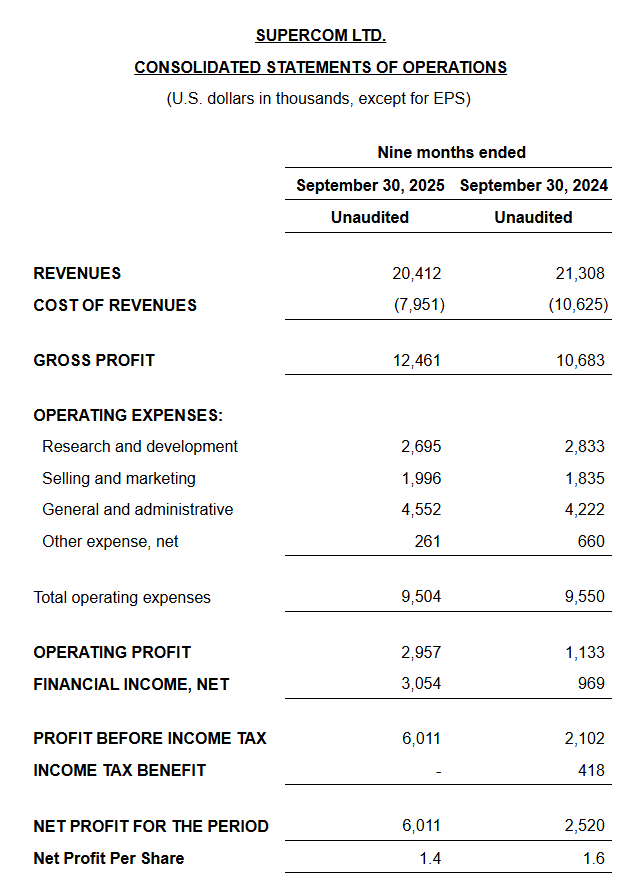

SuperCom has won 65% of all national government tenders it has entered in Europe, proving that its technology and affordability consistently outperform the competition. Despite this competitive edge, the market cap of $38m is only four times the annualized Q3 2025 YTD EBITDA of $7.2m. Additionally, the company has successfully cleaned up its balance sheet; it currently holds approximately $13m in cash and $26m in receivables against only $21m in debt.

What the Company Actually Does

It’s not just about the hardware; it is about their full tech suite called PureSecurity. Their flagship is the PureOne, an all-in-one GPS tracking bracelet that doesn’t need a separate, bulky handheld unit. They also offer the PureTag, which is a tiny RF bracelet for house arrest that has a four-year battery life. This can be compared to typical competitor devices that usually only last one to two days before needing a charge. If an offender forgets to charge their device, it triggers an alert and wastes police time, making SuperCom’s long battery life a major selling point.

They also offer PureProtect, a smartphone app for domestic violence victims that alerts them and the police if an offender gets too close, and PureMonitor, their cloud software that tracks everyone in real-time with inclusion and exclusion zones.

The Turnaround: Moving Past an “Ugly” History

One reason I believe the company is overlooked, aside from it being a nano cap, is because it has had a difficult past. It has a history of unprofitability and massive dilution that scares off most investors.

The company started in 1988 as an “e-gov” company, helping governments manage identity documents like biometric passports and national IDs. They went public on the Nasdaq in 2016 and raised money to grow through acquisitions, such as LCA, which remains a large part of the business today. The problem was that the former CEO, Arie Trabelsi, didn’t focus on one segment; instead, he tried to grow the e-gov, cybersecurity, and electronic monitoring segments simultaneously.

The main issue was that their largest segment at the time, e-gov, relied on contracts that weren’t recurring. These were mostly project-based: once passports were delivered, the revenue stopped. Between 2014 and 2020, revenue fell from ~$30m to $12m and losses kept on rising as contracts were completed and new ones were not secured. Furthermore, they had issued a significant amount of debt to fund acquisitions.

In 2021, a change was necessary. Arie’s son, Ordan Trabelsi, took over as CEO. He had previously grown the U.S. division from zero to $10m and recognized that the future lay in the recurring service fees of electronic monitoring. He performed the difficult task of reverse splits and equity raises to pay down the debt and refocus the entire company on the electronic monitoring segment. By focusing on their strongest segment, they turned profitable in 2024, reporting $6m in net income for the first nine months of 2025.

European vs. U.S. Business Models

If you look at the 2024 and 2025 figures, growth seems to have flattened or even declined slightly, which looks worrying at first glance. However, I believe this is due to the timing of contracts, revenue recognition, and a shift in their business model.

In Europe, SuperCom wins large national-level contracts, such as their $33m deal in Romania. These are usually “front-loaded,” meaning the government makes a large initial order for the monitoring devices, followed by monthly service fees. Under ASC 606 accounting, SuperCom uses a “cost-based” method. If they spend 80% of the total estimated project cost at the beginning of the contracts to produce and deliver the bracelets, they account for 80% of the revenue at that time.

Because that massive Romania contract was signed in August 2022, the 2023 and 2024 figures were heavily inflated by the big initial hardware orders. To do some napkin math: if 80% of that $33m contract hit in the first two years, that is $26.4m in revenue accounted for mostly in 2023 and 2024. This proves to be quite accurate; in 2023 and 2024, respectively 50% (~$13m) and 53% (~$14m) of sales came from one customer, which almost certainly represents the Romania project.

This means 2023 and 2024 numbers are heavily skewed by one contract. Furthermore, this is also why there are so many receivables on the balance sheet; they’ve “earned” the revenue on paper by delivering the gear, but the government pays it out over time.

The Shift to the U.S. Market

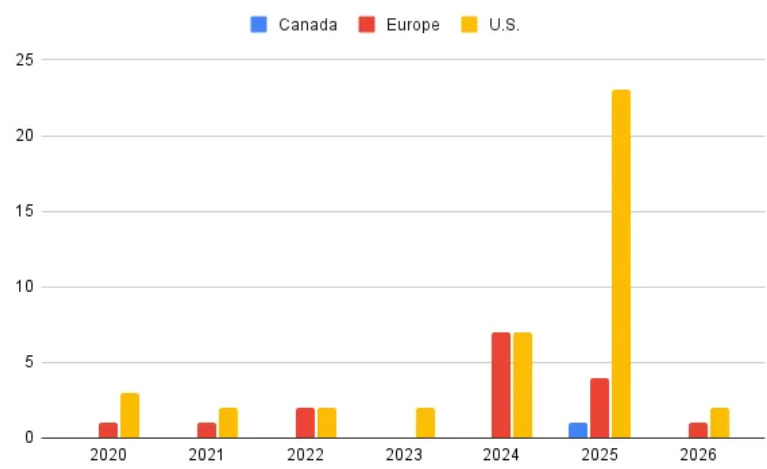

In 2024 and 2025, they refocused on the U.S. market, where the business model is much more favorable. Instead of large up-front orders, the U.S. works on a leasing model where SuperCom gets a steady recurring fee of about $2,900 per offender annually. Below you can see the number of announced won contracts by geography.

I believe that currently, a much larger part of their revenue comes from the U.S. and this shift is the primary driver behind the rapid expansion of gross margins. A look at the gross margins for 2023, 2024, and 2025 reveals a clear upward trajectory: 38%, 48%, and 62% (YTD) respectively. This trend confirms that revenue is shifting toward the high-margin U.S. leasing model and away from one-time hardware sales in Europe.

The reason for reported revenues not increasing is that ~80% of the Romanian contract has already been recognized. In 2025, the revenue contribution will be significantly lower. Given the four-year contract length and the remaining 20% to be recognized, I estimate it will contribute roughly $3m (10%) in revenue for 2025. When excluding the Romanian deal from the YTD Q3 figures, revenue grew from $10m in 2024 to $18m in 2025. This represents an 80% growth rate in the underlying business. These figures, combined with expanding margins, offer strong evidence that the U.S. market is growing rapidly and that the underlying economics are highly attractive. Furthermore, the U.S. electronic monitoring market is six times larger than the European market, offering substantially more potential.

Industry Dynamics and Moats

In this industry, trust is everything. As the company builds its reputation, it becomes easier to secure more frequent and larger deals. Government agencies are often hesitant to award large contracts to a new player; however, once trust is established in a specific country or state, it becomes much easier to secure larger follow-on contracts. Since mid-2024, they have won over 35 new contracts across 15 different states.

Here are some examples of this dynamic:

Sweden: In March 2026, they won a $17m national contract, displacing an incumbent that had been there for 25 years. This new contract is 2.5 times larger than their previous contract in Sweden.

Kentucky: They won their first contract in mid-2024, and as of March 2026, they have announced their fourth contract win in the state.

Additionally, there are significant barriers to entry. According to management, five to ten years of specific industry experience is typically required just to bid on government tenders in this market.

Sector Tailwinds

Beyond the fact that SuperCom is disrupting the industry, the electronic monitoring market is expected to grow at a CAGR of 7.2% until 2028. There are two main drivers of this growth:

Cost: Placing a person under house arrest costs about $2,900 annually, while incarceration costs $36,500. The potential savings for governments are massive.

Capacity: U.S. prisons are currently overcrowded, with 103% occupancy.

Valuation and Outlook

Creating an accurate model is difficult because the sizes of most announced contracts are not disclosed, and cost-based accounting skews the figures. However, the valuation remains compelling. The company has a clean balance sheet with $13m in cash and $26m in receivables, against liabilities of about $28m.

I believe the company is on track to outperform the broader market. Li’l Oaty, who provides excellent coverage of SuperCom, estimates that 2026 growth will fall between 25% and 40%. I find his estimation to be quite reasonable, especially considering the core business is growing at 80% when excluding the Romanian deal.

On the earnings side, I calculated a normalized FCF by taking EBITDA and subtracting cash interest payments, stock-based compensation (which I treat as an expense), taxes, capex, and capitalized R&D. This results in approximately $4m in normalized FCF for 2025, representing a 9.5x FCF multiple. As the company scales and the U.S. segment becomes a larger portion of total revenue, I expect both FCF conversion and margins to improve further. While their debt matures in December 2028, SuperCom is well-positioned to retire these obligations using its existing cash balance and ongoing operational cash flow.

Ultimately, this is a company trading at single-digit earnings that is poised for high growth. My thought process is that within two to three years, we will likely see revenues double, margins expand, and valuation multiples re-rate higher. This gives me confidence that SuperCom has a clear path to becoming a multibagger over the medium term.

For those interested in a deeper dive, Li’l Oaty’s extensive write-up is an excellent resource that goes into much more detail. I also suggest following the $SPCB ticker on X to find a lot of smart people doing great research. This includes tracking new potential contract wins before they are officially announced.

Nice thoughts, I hadn’t dug into the accounting nuances much myself. It’s funny, I’d say >80% of the people I mention this name to take one look at the historical earnings and stock issuance and are immediately like “yeah I’ll pass”. I definitely think getting some profitable numbers with more visibility into the “we don’t have to issue more stock” story will be the key to get more people excited about this name. In the meantime, good to be early if it works out :)